RDSP vs. TFSA vs. RRSP: Which Account Is Right for Someone with a Disability?

RDSP vs. TFSA vs. RRSP: Which Account Is Right for Someone with a Disability?

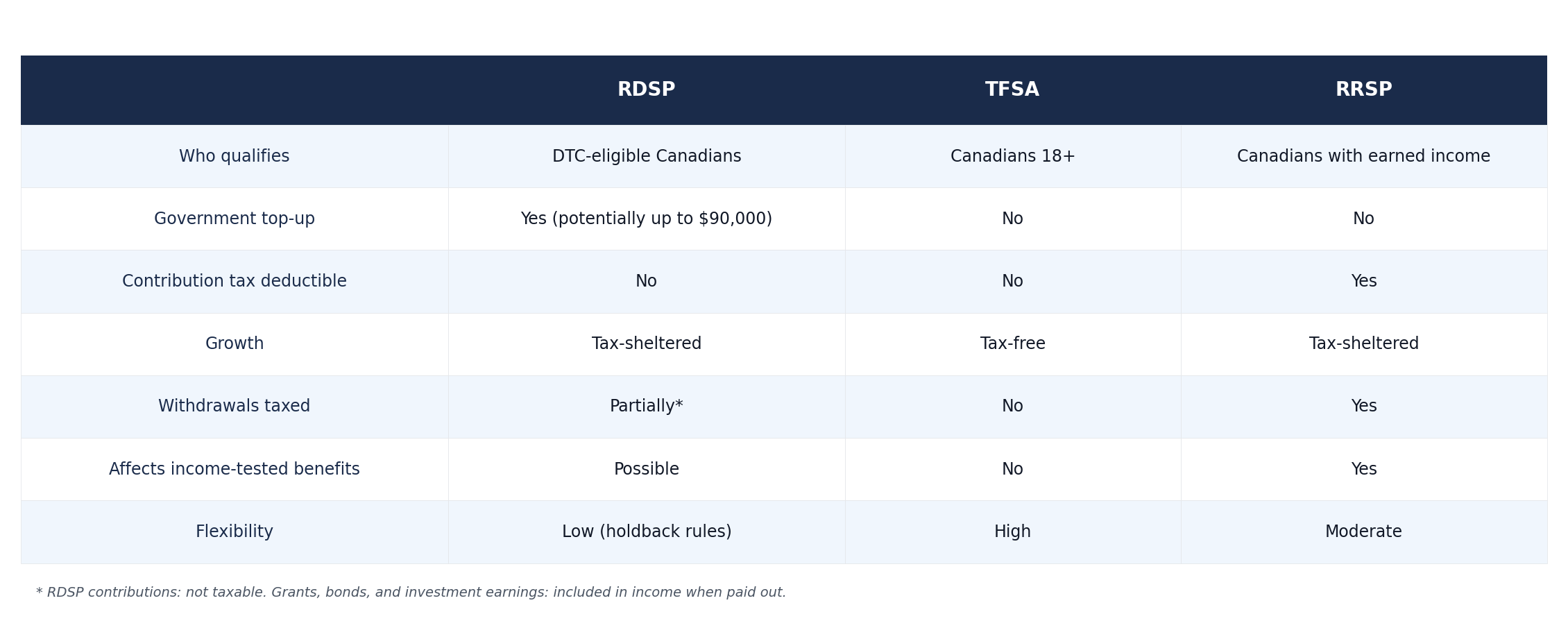

For Canadians living with a disability, or families planning ahead for a loved one, three registered savings accounts come up most often: the Registered Disability Savings Plan (RDSP), the Tax-Free Savings Account (TFSA), and the Registered Retirement Savings Plan (RRSP).

All three are powerful tools. But they work very differently. Choosing the right one starts with understanding what each account is actually designed to do, and how the government supports each of them.

The RDSP: The Account Built Specifically for Disability

The Registered Disability Savings Plan exists for one purpose: to help Canadians with severe and prolonged disabilities save for long-term financial security.

What makes it unique is the government money attached to it.

Canada Disability Savings Grants (CDSGs): The federal government matches your contributions with grants of up to $3,500 per year, depending on your family income. Over a lifetime, a beneficiary can receive up to $70,000 in total grants.

Canada Disability Savings Bonds (CDSBs): For lower-income Canadians, the government deposits up to $1,000 per year into the RDSP even if you contribute nothing yourself. The lifetime bond maximum is $20,000.

That is potentially up to $90,000 in federal grants and bonds over a lifetime, an amount that no other registered account comes close to matching. Grant and bond eligibility is income-tested and uses prior-year family net income for calculations.

To open an RDSP, the beneficiary must qualify for the Disability Tax Credit (DTC) and be under age 60 when the plan is opened. Contributions can be made until the end of the year the beneficiary turns 59. The DTC is a federal tax credit for Canadians with a severe and prolonged physical or mental impairment. If it has not yet been applied for, that is the first step.

Contribution rules: There is no annual contribution limit for the RDSP, but the lifetime contribution limit is $200,000. Contributions are not tax-deductible. However, growth inside the plan, including grants and bonds, is tax-sheltered until withdrawn.

Withdrawals: Regular RDSP withdrawals are called Lifetime Disability Assistance Payments (LDAPs) and must begin by age 60. When withdrawn, your original contributions are not taxable, but grants, bonds, and investment earnings are included in the beneficiary's income. There are also holdback rules tied to grants and bonds received in the preceding 10 years, meaning early withdrawals can trigger repayment of some government assistance. This account is designed to be held long-term.

The TFSA: The Flexible All-Purpose Account

The Tax-Free Savings Account is available to any Canadian who is 18 or older and has a valid Social Insurance Number. It does not require any medical qualification.

Money grows inside a TFSA completely tax-free, and withdrawals are also tax-free, at any time, for any reason. That flexibility is what sets the TFSA apart.

Annual contribution room: The TFSA has an annual contribution limit set by the federal government each year (currently $7,000 for 2026). Unused room carries forward from previous years. Anyone who was 18 or older in 2009, when the TFSA was introduced, has accumulated significant room over time. Withdrawn amounts are added back to contribution room on January 1 of the following year.

No income impact: This is a key advantage for Canadians with disabilities. TFSA withdrawals are not included in income and do not affect federal income-tested benefits or credits. Provincial programs may have their own rules, so it is worth checking how your specific benefits are calculated. That is a significant distinction for anyone receiving disability-related assistance.

No withdrawal restrictions: Unlike the RDSP, there are no holdback rules or minimum holding periods. Money can be withdrawn and re-contributed in future years.

For someone with a disability who needs flexible access to savings, or who relies on income-tested benefits that could be disrupted by taxable income, the TFSA is often the most practical day-to-day savings vehicle.

The RRSP: The Tax-Deferred Retirement Account

The Registered Retirement Savings Plan is Canada's primary retirement savings vehicle. Contributions are tax-deductible, meaning they reduce your taxable income in the year you contribute. Growth inside the plan is tax-sheltered, and withdrawals are taxed as income when taken out.

Contribution room: RRSP room is based on earned income, 18% of your prior year's earned income, up to an annual maximum. If you have little or no earned income, you accumulate little or no RRSP room.

Important consideration for disability recipients: Many Canadians with disabilities receive income from provincial disability programs, the Canada Pension Plan Disability benefit (CPP-D), or other sources. Whether those count as earned income for RRSP purposes depends on the source. CPP-D payments, for example, do count as earned income and generate RRSP room, while most provincial disability assistance payments do not.

Withdrawals count as income: Unlike TFSA withdrawals, RRSP withdrawals are fully taxable. RRSP withdrawals are taxable and may affect income-tested benefits and tax rates, depending on the program and the individual's situation. Spousal RRSP: If a person with a disability has a spouse or partner, a spousal RRSP contribution can be a way to split income in retirement and manage taxation more effectively.

How to Use All Three Together

For most Canadians with a disability, the RDSP should come first, specifically to capture the government grants and bonds. The free money attached to this account is hard to beat, and it is available only while the beneficiary is under 49 (grants and bonds stop after age 49).

The TFSA fills the gap for flexible savings, money that may be needed in the short to medium term, and that must not count as income for benefit purposes.

The RRSP makes the most sense for those who have meaningful earned income, are in a higher tax bracket, and can benefit from the deduction. It becomes less useful when withdrawals could disrupt income-tested benefits.

None of these accounts need to be used exclusively. Many Canadians with disabilities use all three, prioritizing RDSP contributions first to capture government assistance, building TFSA savings for flexibility, and using the RRSP selectively based on their income situation in a given year.

One Step That Often Gets Missed

If a loved one with a disability does not yet have the Disability Tax Credit on file, applying for it is the first step to unlocking the RDSP, including retroactive grants and bonds that may be available based on past eligibility.

The DTC application goes through the Canada Revenue Agency and requires certification from a medical practitioner. Once approved, the RDSP can be opened, and the catch-up grants process can begin.

This content is provided for general informational purposes only. It is not intended to provide investment, tax, or legal advice, and should not be relied upon as such. Sources: